- Joined

- 12/6/18

- Messages

- 26

- Points

- 13

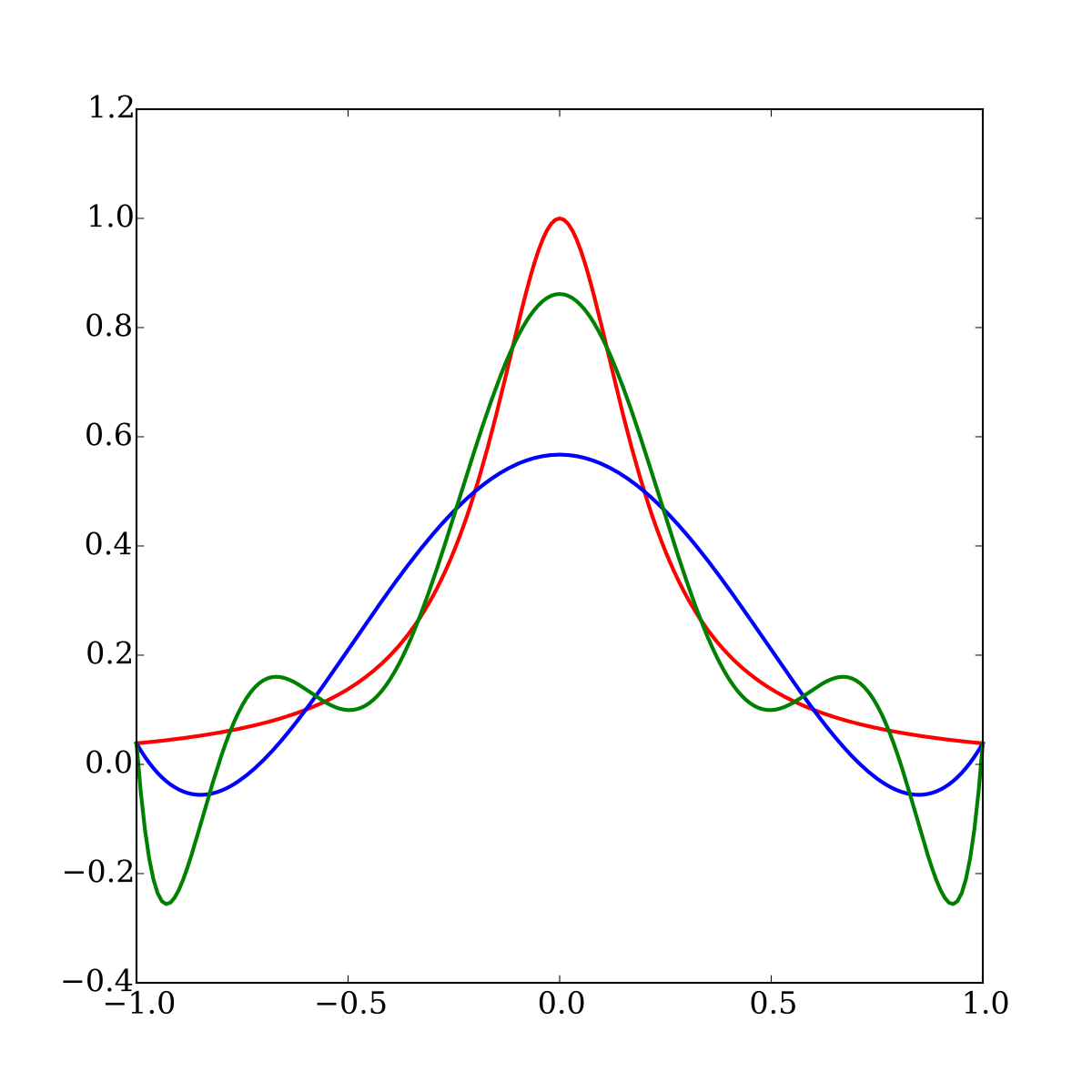

I just published with my colleague Brian Huge the result of 6m+ research at Danske Bank on pricing and risk approximation by AI. We found that the combination of ML with automatic differentiation (AAD) makes a rather spectacular difference.

working paper: [2005.02347] Differential Machine Learning

gitHub: differential-machine-learning - Overview

colab notebook: Google Colaboratory

blog: Differential Machine Learning

Antoine Savine

The working paper is available on arXiv, pending review by Risk Magazine. Feedback from the community is much appreciated.working paper: [2005.02347] Differential Machine Learning

gitHub: differential-machine-learning - Overview

colab notebook: Google Colaboratory

blog: Differential Machine Learning

Antoine Savine

") Start with the Machine Learning course, and carry on with the Deep Learning specialization.

Start with the Machine Learning course, and carry on with the Deep Learning specialization.