- Joined

- 5/2/06

- Messages

- 11,763

- Points

- 273

If You Know Options, You’re Likely to Know Stocks

By MARK HULBERT

Published: August 13, 2006

DO options traders know more about buying and selling stocks than the rest of us?

It seems that much of the time, they do. A new study has found that a portfolio based on the preferences of options traders has consistently beaten the overall stock market. In reaching that conclusion, the study paves the way for what may be a very profitable stock-picking strategy.

The study, "The Information in Option Volume for Future Stock Prices," appears in the fall 2006 issue of the Review of Financial Studies. Its authors are two associate professors of finance: Jun Pan of the Sloan School of Management at the Massachusetts Institute of Technology and Allen M. Poteshman of the University of Illinois at Urbana-Champaign.

Because of the way options are designed, traders have powerful incentives to go to the options market when they have information that is likely to affect a stock's price, Professor Poteshman said. A call option, for example, which amounts to a bet that a stock's price will rise, enables its owner to buy that stock at a predetermined level. If, by the time of the option's expiration, the stock trades above that level, the option may be worth several times what was paid for it; if not, it will be worthless. In other words, the option has much leverage. As a result, a small percentage change in the price of the underlying stock can mean a difference of hundreds of percentage points in the option's profitability.

Similar risks and rewards exist for put options, which are bets that a stock's price will fall. Puts enable their owners to sell that stock at a preset level, and will be worth an increasingly large amount if the stock trades below that level by the time that put expires. If not, the put will be worthless.

Until now, there has been no comprehensive study of option traders' track records as stock pickers. That hasn't been for want of trying: the requisite data simply was not available to researchers. The volume figures that options exchanges report publicly, for example, reflect a combination of several kinds of transactions, muddying the overall picture. The volume number reported for a given option, for example, may reflect new purchases by options traders, but it may also include the sale of positions previously acquired. That makes it hard to tell whether traders actually favored a stock.

Using a private database provided by the Chicago Board Options Exchange, the two professors were able to deconstruct an option's total trading volume into various categories. They excluded trades by market makers, for example — dealers at the options exchange who buy and sell securities for the general purpose of maintaining liquidity. They narrowed the database further to focus on just that portion of an option's daily trading volume that reflected new positions by other traders, on the assumption that these transactions offered a clearer signal of what traders actually thought of the underlying stock. The database covered the dozen years from the beginning of 1990 through the end of 2001.

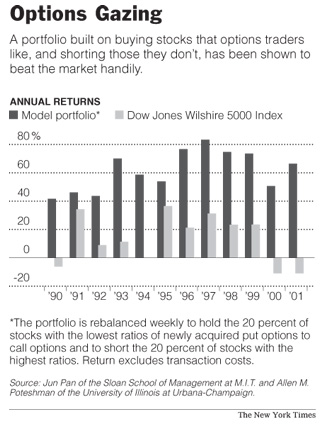

For each option in this database, the professors calculated a daily volume ratio of newly acquired put options to newly acquired call options. A high ratio meant a strong consensus among options traders that the price of the option's underlying stock would fall, while a low ratio showed a widely shared expectation that the stock would rise. The professors found that the stocks whose options had the lowest ratios consistently outperformed the stocks whose options had the highest ratios.

Consider this hypothetical portfolio constructed by the professors: it held the stocks of the 20 percent of options with the lowest put-call ratios, while selling short the stocks whose options had the highest such ratios. (The portfolio was readjusted weekly, adding and deleting stocks because of changes in the ratios.)

The professors reported that before transaction costs, this portfolio produced an annual average return of 62 percent over the dozen years covered in the study. This contrasts with an annualized total return of 12.3 percent for the general stock market over this period, as measured by the Dow Jones Wilshire 5000 index. Still more impressive was the fact that the portfolio earned double-digit returns each year, even when the overall market declined. Based on their data, however, the professors had no way to determine how options traders were able to achieve these results.

The portfolio required frequent transactions because the price moves correctly anticipated by options traders lasted for only a couple of weeks, on average. So transaction costs would have eaten up a big chunk of the return. But Professor Poteshman estimated that in the hands of an institutional investor, for whom such costs would typically be quite low, the portfolio's return would still have been as much as 50 percent annually.

Even for individual investors, who would pay higher costs, Professor Poteshman estimated that the annualized return would have been well into double digits.

DESPITE the strong results of the strategy, it would have no more than academic interest if investors had no access to the private C.B.O.E. database that the professors studied. In July, however, the exchange began selling subscriptions to this database to the public.

A subscription isn't cheap: $600 a month. That helps make the professors' strategy impractical for small investors. Still, the study shows that potentially valuable information can be found in options traders' behavior. And institutional investors, including hedge funds and mutual funds, can easily exploit it.

By MARK HULBERT

Published: August 13, 2006

DO options traders know more about buying and selling stocks than the rest of us?

It seems that much of the time, they do. A new study has found that a portfolio based on the preferences of options traders has consistently beaten the overall stock market. In reaching that conclusion, the study paves the way for what may be a very profitable stock-picking strategy.

The study, "The Information in Option Volume for Future Stock Prices," appears in the fall 2006 issue of the Review of Financial Studies. Its authors are two associate professors of finance: Jun Pan of the Sloan School of Management at the Massachusetts Institute of Technology and Allen M. Poteshman of the University of Illinois at Urbana-Champaign.

Because of the way options are designed, traders have powerful incentives to go to the options market when they have information that is likely to affect a stock's price, Professor Poteshman said. A call option, for example, which amounts to a bet that a stock's price will rise, enables its owner to buy that stock at a predetermined level. If, by the time of the option's expiration, the stock trades above that level, the option may be worth several times what was paid for it; if not, it will be worthless. In other words, the option has much leverage. As a result, a small percentage change in the price of the underlying stock can mean a difference of hundreds of percentage points in the option's profitability.

Similar risks and rewards exist for put options, which are bets that a stock's price will fall. Puts enable their owners to sell that stock at a preset level, and will be worth an increasingly large amount if the stock trades below that level by the time that put expires. If not, the put will be worthless.

Until now, there has been no comprehensive study of option traders' track records as stock pickers. That hasn't been for want of trying: the requisite data simply was not available to researchers. The volume figures that options exchanges report publicly, for example, reflect a combination of several kinds of transactions, muddying the overall picture. The volume number reported for a given option, for example, may reflect new purchases by options traders, but it may also include the sale of positions previously acquired. That makes it hard to tell whether traders actually favored a stock.

Using a private database provided by the Chicago Board Options Exchange, the two professors were able to deconstruct an option's total trading volume into various categories. They excluded trades by market makers, for example — dealers at the options exchange who buy and sell securities for the general purpose of maintaining liquidity. They narrowed the database further to focus on just that portion of an option's daily trading volume that reflected new positions by other traders, on the assumption that these transactions offered a clearer signal of what traders actually thought of the underlying stock. The database covered the dozen years from the beginning of 1990 through the end of 2001.

For each option in this database, the professors calculated a daily volume ratio of newly acquired put options to newly acquired call options. A high ratio meant a strong consensus among options traders that the price of the option's underlying stock would fall, while a low ratio showed a widely shared expectation that the stock would rise. The professors found that the stocks whose options had the lowest ratios consistently outperformed the stocks whose options had the highest ratios.

Consider this hypothetical portfolio constructed by the professors: it held the stocks of the 20 percent of options with the lowest put-call ratios, while selling short the stocks whose options had the highest such ratios. (The portfolio was readjusted weekly, adding and deleting stocks because of changes in the ratios.)

The professors reported that before transaction costs, this portfolio produced an annual average return of 62 percent over the dozen years covered in the study. This contrasts with an annualized total return of 12.3 percent for the general stock market over this period, as measured by the Dow Jones Wilshire 5000 index. Still more impressive was the fact that the portfolio earned double-digit returns each year, even when the overall market declined. Based on their data, however, the professors had no way to determine how options traders were able to achieve these results.

The portfolio required frequent transactions because the price moves correctly anticipated by options traders lasted for only a couple of weeks, on average. So transaction costs would have eaten up a big chunk of the return. But Professor Poteshman estimated that in the hands of an institutional investor, for whom such costs would typically be quite low, the portfolio's return would still have been as much as 50 percent annually.

Even for individual investors, who would pay higher costs, Professor Poteshman estimated that the annualized return would have been well into double digits.

DESPITE the strong results of the strategy, it would have no more than academic interest if investors had no access to the private C.B.O.E. database that the professors studied. In July, however, the exchange began selling subscriptions to this database to the public.

A subscription isn't cheap: $600 a month. That helps make the professors' strategy impractical for small investors. Still, the study shows that potentially valuable information can be found in options traders' behavior. And institutional investors, including hedge funds and mutual funds, can easily exploit it.