Hi,

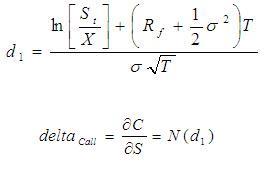

I have a problem with the Delta-Gamma approximation to calculate changes in value of a portfolio.

I think I got something wrong but at the moment I don't see the mistake.

My example portfolio is only consisting of an call option.

I calculate dV with the formula for the Delta-Gamma approximation.

Maturity T=0.5 , starting point is t=0 and the portfolio revaluation occurs in t=0.1. Furthermore r=0, K=100, S(0)=100, sigma=10% and I assume the stock price at t=0.1 to be 105.

To compare, I first calculate the Black-Scholes price in t=0 and then in t=0.1 . Then the difference should be the change in value, right?

My results were: dV=3 for the BS method and dV=2,486 for the Delta-Gamma-approx.

I don't think that the approximation should lead to such a huge error.

Hopefully, someone can help me out!

Thanks in advance.

I have a problem with the Delta-Gamma approximation to calculate changes in value of a portfolio.

I think I got something wrong but at the moment I don't see the mistake.

My example portfolio is only consisting of an call option.

I calculate dV with the formula for the Delta-Gamma approximation.

Maturity T=0.5 , starting point is t=0 and the portfolio revaluation occurs in t=0.1. Furthermore r=0, K=100, S(0)=100, sigma=10% and I assume the stock price at t=0.1 to be 105.

To compare, I first calculate the Black-Scholes price in t=0 and then in t=0.1 . Then the difference should be the change in value, right?

My results were: dV=3 for the BS method and dV=2,486 for the Delta-Gamma-approx.

I don't think that the approximation should lead to such a huge error.

Hopefully, someone can help me out!

Thanks in advance.

")

")