Op-Ed piece from NYT

Innovating Our Way to Financial Crisis

By PAUL KRUGMAN

Published: December 3, 2007

The financial crisis that began late last summer, then took a brief vacation in September and October, is back with a vengeance.

Paul Krugman.

How bad is it? Well, I've never seen financial insiders this spooked — not even during the Asian crisis of 1997-98, when economic dominoes seemed to be falling all around the world.

This time, market players seem truly horrified — because they've suddenly realized that they don't understand the complex financial system they created.

Before I get to that, however, let's talk about what's happening right now.

Credit — lending between market players — is to the financial markets what motor oil is to car engines. The ability to raise cash on short notice, which is what people mean when they talk about "liquidity," is an essential lubricant for the markets, and for the economy as a whole.

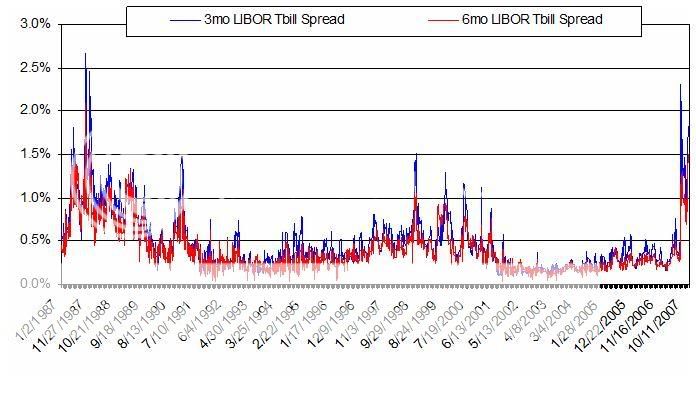

But liquidity has been drying up. Some credit markets have effectively closed up shop. Interest rates in other markets — like the London market, in which banks lend to each other — have risen even as interest rates on U.S. government debt, which is still considered safe, have plunged.

"What we are witnessing," says Bill Gross of the bond manager Pimco, "is essentially the breakdown of our modern-day banking system, a complex of leveraged lending so hard to understand that Federal Reserve Chairman Ben Bernanke required a face-to-face refresher course from hedge fund managers in mid-August."

The freezing up of the financial markets will, if it goes on much longer, lead to a severe reduction in overall lending, causing business investment to go the way of home construction — and that will mean a recession, possibly a nasty one.

Behind the disappearance of liquidity lies a collapse of trust: market players don't want to lend to each other, because they're not sure they'll be repaid.

In a direct sense, this collapse of trust has been caused by the bursting of the housing bubble. The run-up of home prices made even less sense than the dot-com bubble — I mean, there wasn't even a glamorous new technology to justify claims that old rules no longer applied — but somehow financial markets accepted crazy home prices as the new normal. And when the bubble burst, a lot of investments that were labeled AAA turned out to be junk.

Thus, "super-senior" claims against subprime mortgages — that is, investments that have first dibs on whatever mortgage payments borrowers make, and were therefore supposed to pay off in full even if a sizable fraction of these borrowers defaulted on their debts — have lost a third of their market value since July.

But what has really undermined trust is the fact that nobody knows where the financial toxic waste is buried. Citigroup wasn't supposed to have tens of billions of dollars in subprime exposure; it did. Florida's Local Government Investment Pool, which acts as a bank for the state's school districts, was supposed to be risk-free; it wasn't (and now schools don't have the money to pay teachers).

How did things get so opaque? The answer is "financial innovation" — two words that should, from now on, strike fear into investors' hearts.

O.K., to be fair, some kinds of financial innovation are good. I don't want to go back to the days when checking accounts didn't pay interest and you couldn't withdraw cash on weekends.

But the innovations of recent years — the alphabet soup of C.D.O.'s and S.I.V.'s, R.M.B.S. and A.B.C.P. — were sold on false pretenses. They were promoted as ways to spread risk, making investment safer. What they did instead — aside from making their creators a lot of money, which they didn't have to repay when it all went bust — was to spread confusion, luring investors into taking on more risk than they realized.

Why was this allowed to happen? At a deep level, I believe that the problem was ideological: policy makers, committed to the view that the market is always right, simply ignored the warning signs. We know, in particular, that Alan Greenspan brushed aside warnings from Edward Gramlich, who was a member of the Federal Reserve Board, about a potential subprime crisis.

And free-market orthodoxy dies hard. Just a few weeks ago Henry Paulson, the Treasury secretary, admitted to Fortune magazine that financial innovation got ahead of regulation — but added, "I don't think we'd want it the other way around." Is that your final answer, Mr. Secretary?

Now, Mr. Paulson's new proposal to help borrowers renegotiate their mortgage payments and avoid foreclosure sounds in principle like a good idea (although we have yet to hear any details). Realistically, however, it won't make more than a small dent in the subprime problem.

The bottom line is that policy makers left the financial industry free to innovate — and what it did was to innovate itself, and the rest of us, into a big, nasty mess.

Innovating Our Way to Financial Crisis

By PAUL KRUGMAN

Published: December 3, 2007

The financial crisis that began late last summer, then took a brief vacation in September and October, is back with a vengeance.

Paul Krugman.

How bad is it? Well, I've never seen financial insiders this spooked — not even during the Asian crisis of 1997-98, when economic dominoes seemed to be falling all around the world.

This time, market players seem truly horrified — because they've suddenly realized that they don't understand the complex financial system they created.

Before I get to that, however, let's talk about what's happening right now.

Credit — lending between market players — is to the financial markets what motor oil is to car engines. The ability to raise cash on short notice, which is what people mean when they talk about "liquidity," is an essential lubricant for the markets, and for the economy as a whole.

But liquidity has been drying up. Some credit markets have effectively closed up shop. Interest rates in other markets — like the London market, in which banks lend to each other — have risen even as interest rates on U.S. government debt, which is still considered safe, have plunged.

"What we are witnessing," says Bill Gross of the bond manager Pimco, "is essentially the breakdown of our modern-day banking system, a complex of leveraged lending so hard to understand that Federal Reserve Chairman Ben Bernanke required a face-to-face refresher course from hedge fund managers in mid-August."

The freezing up of the financial markets will, if it goes on much longer, lead to a severe reduction in overall lending, causing business investment to go the way of home construction — and that will mean a recession, possibly a nasty one.

Behind the disappearance of liquidity lies a collapse of trust: market players don't want to lend to each other, because they're not sure they'll be repaid.

In a direct sense, this collapse of trust has been caused by the bursting of the housing bubble. The run-up of home prices made even less sense than the dot-com bubble — I mean, there wasn't even a glamorous new technology to justify claims that old rules no longer applied — but somehow financial markets accepted crazy home prices as the new normal. And when the bubble burst, a lot of investments that were labeled AAA turned out to be junk.

Thus, "super-senior" claims against subprime mortgages — that is, investments that have first dibs on whatever mortgage payments borrowers make, and were therefore supposed to pay off in full even if a sizable fraction of these borrowers defaulted on their debts — have lost a third of their market value since July.

But what has really undermined trust is the fact that nobody knows where the financial toxic waste is buried. Citigroup wasn't supposed to have tens of billions of dollars in subprime exposure; it did. Florida's Local Government Investment Pool, which acts as a bank for the state's school districts, was supposed to be risk-free; it wasn't (and now schools don't have the money to pay teachers).

How did things get so opaque? The answer is "financial innovation" — two words that should, from now on, strike fear into investors' hearts.

O.K., to be fair, some kinds of financial innovation are good. I don't want to go back to the days when checking accounts didn't pay interest and you couldn't withdraw cash on weekends.

But the innovations of recent years — the alphabet soup of C.D.O.'s and S.I.V.'s, R.M.B.S. and A.B.C.P. — were sold on false pretenses. They were promoted as ways to spread risk, making investment safer. What they did instead — aside from making their creators a lot of money, which they didn't have to repay when it all went bust — was to spread confusion, luring investors into taking on more risk than they realized.

Why was this allowed to happen? At a deep level, I believe that the problem was ideological: policy makers, committed to the view that the market is always right, simply ignored the warning signs. We know, in particular, that Alan Greenspan brushed aside warnings from Edward Gramlich, who was a member of the Federal Reserve Board, about a potential subprime crisis.

And free-market orthodoxy dies hard. Just a few weeks ago Henry Paulson, the Treasury secretary, admitted to Fortune magazine that financial innovation got ahead of regulation — but added, "I don't think we'd want it the other way around." Is that your final answer, Mr. Secretary?

Now, Mr. Paulson's new proposal to help borrowers renegotiate their mortgage payments and avoid foreclosure sounds in principle like a good idea (although we have yet to hear any details). Realistically, however, it won't make more than a small dent in the subprime problem.

The bottom line is that policy makers left the financial industry free to innovate — and what it did was to innovate itself, and the rest of us, into a big, nasty mess.