- Joined

- 5/28/23

- Messages

- 15

- Points

- 13

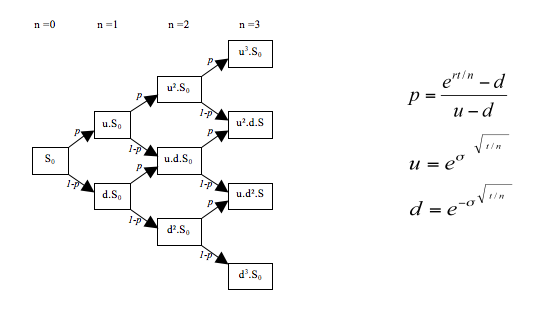

from the book it is using below

Whick look different than the common one(which we learn in CFA

en.wikipedia.org

en.wikipedia.org

Wonder if they are same model, but just different presentation,

or above one is move advance?

double dt = T/N; double nu = r - 0.5*sig*sig; // Up and down jumps double dxu = std::sqrt(sig*sig*dt + (nu*dt)*(nu*dt)); double dxd = -dxu; // Corresponding probabilities double pu = 0.5 + 0.5*(nu*dt/dxu); double pd = 1.0 - pu; // Precompute constants double disc = std::exp(-r*dt); double dpu = disc*pu; double dpd = disc*pd; double edxud = std::exp(dxu - dxd); double edxd = std::exp(dxd);Whick look different than the common one(which we learn in CFA

Lattice model (finance) - Wikipedia

Wonder if they are same model, but just different presentation,

or above one is move advance?

Last edited: