When calculating the option prices with the use of finite difference methods you approximate the derivatives in the Black & Scholes PDE.

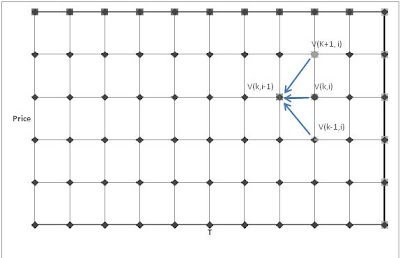

Where do you get the option prices used in these approximations? I mean, we are supposed to calculate the option price, and at the same time you need prices to do the approximations of the derivatives.

Also, what is x in the BS PDE du/dt = 1/2 * sigma^2 * d^u/dx^2?

Thanks in advance.

Where do you get the option prices used in these approximations? I mean, we are supposed to calculate the option price, and at the same time you need prices to do the approximations of the derivatives.

Also, what is x in the BS PDE du/dt = 1/2 * sigma^2 * d^u/dx^2?

Thanks in advance.