- Joined

- 1/10/11

- Messages

- 124

- Points

- 38

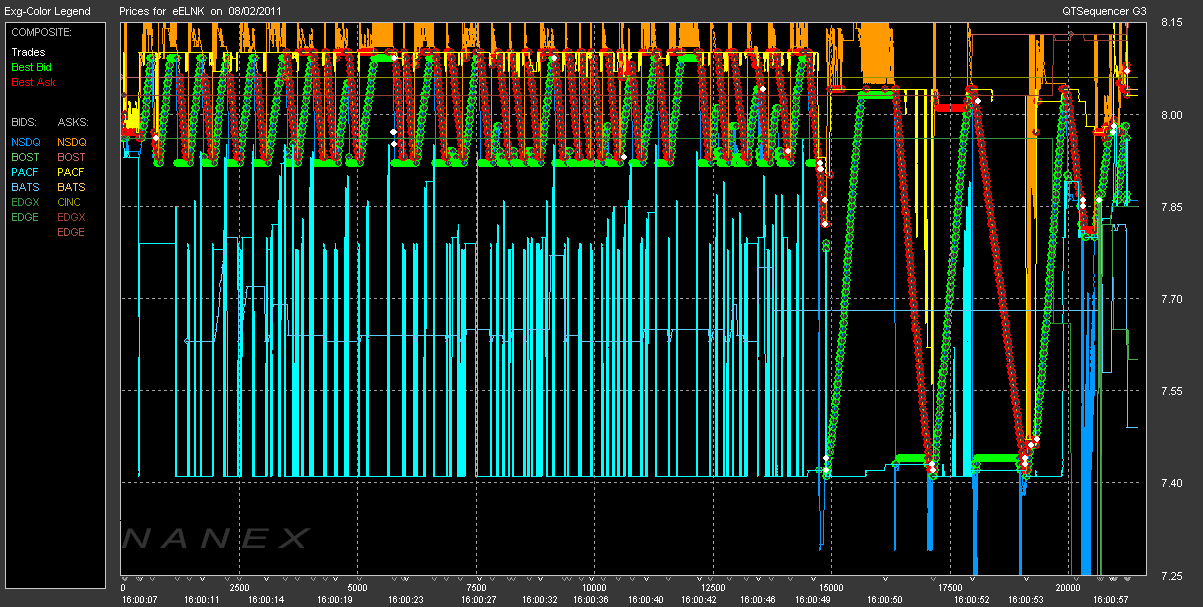

Regulators in the United States and overseas are cracking down on computerized high-speed trading that crowds today’s stock exchanges, worried that as it spreads around the globe it is making market swings worse.

The cost of these high-frequency traders, critics say, is the confidence of ordinary investors in the markets, and ultimately their belief in the fairness of the financial system.

“There is something unholy about them,” said Guy P. Wyser-Pratte, a prominent longtime Wall Street trader and investor. “That is what caused this tremendous volatility. They make a fortune whereas the public gets so whipsawed by this trading.”

http://www.nytimes.com/2011/10/09/business/clamping-down-on-rapid-trades-in-stock-market.html?_r=1