- Joined

- 12/25/20

- Messages

- 13

- Points

- 11

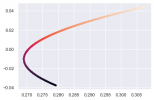

Hi all, could you please help me identify if there is anything wrong in my code? And if nothing is wrong, could you please let me know why the graph looks weird?

Efficient Frontier:

# -*- coding: utf-8 -*-

"""

Created on Wed Jan 13 17:03:13 2021

"""

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set()

from math import *

from scipy.optimize import minimize

pd.set_option('display.max_rows', 10)

pd.set_option('display.max_columns', 10)

import pickle

from pandas_datareader import data as wb

tickers=['F','GM']

data=pd.DataFrame()

for t in tickers:

data[t]=wb.DataReader(t, data_source='yahoo', start='07-5-2012', end='5-7-2020')['Adj Close']

log_returns=np.log(data/data.shift(1))

num_ports=50000

ret_array=np.zeros(num_ports)

all_weights=np.zeros((num_ports, len(data.columns)))

vol_array=np.zeros(num_ports)

sharpe_array=np.zeros(num_ports)

for ind in range(num_ports):

weights=np.random.random(2)

weights=weights/np.sum(weights)

all_weights[ind,:]=weights

ret_array[ind]=np.sum(weights*log_returns.mean()*252)

vol_array[ind]=sqrt(np.dot(weights.T, np.dot(weights, log_returns.cov()*252)))

sharpe_array[ind]=ret_array[ind]/vol_array[ind]

plt.scatter(vol_array, ret_array, c=sharpe_array, s=8)

plt.show()