- Joined

- 2/28/17

- Messages

- 2

- Points

- 11

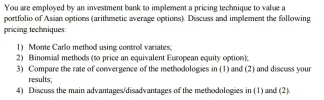

I have this assignement on option pricing on one of my courses. I know the technicalities, but I would really appreciate any suggestions on how to compare the convergence of the methodologies.

Also, any other advice on how I should approach it is welcomed!

Thank you!

Alex

Also, any other advice on how I should approach it is welcomed!

Thank you!

Alex